Skip to content

Skip to content

Wells Fargo (WFC) Stock: Still Cautious Despite Solid Results

Stock: Still Cautious Despite Solid Results")

Michael M. Santiago

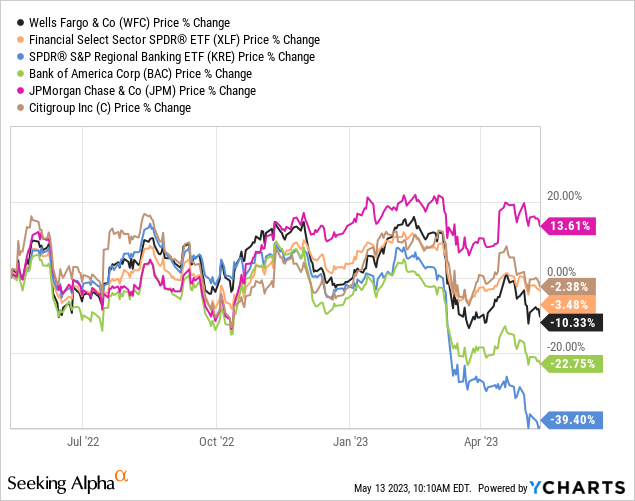

My last article about Wells Fargo (NYSE:WFC) was published at the end of June 2022 and I was not fond of the bank and didn’t see it as a good investment. And as WFC stock is now trading about 5.5% lower, it certainly wasn’t a good investment. But we also must admit that Wells Fargo’s stock performance was better than the performance of Bank of America (BAC) for example and of course than almost every regional bank (by the way: most Canadian banks also had a worse performance).

During the last year, Wells Fargo mostly moved sideways and considering the bank collapses that happened in the last few months, let’s take another look at Wells Fargo if it is a good investment right now and if we should invest in a bank before a potential recession. And of course, we are looking at the financial stability of Wells Fargo but start with the quarterly results.

Quarterly Results

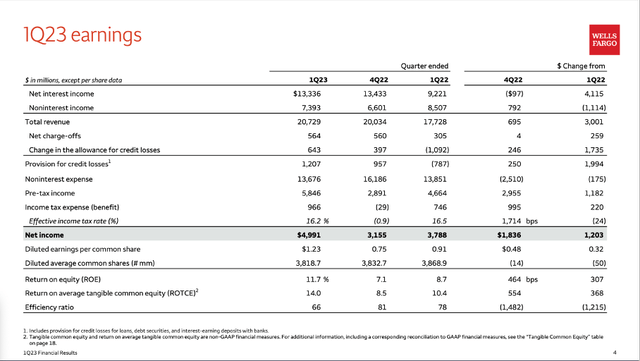

Similar to many other banks, Wells Fargo actually reported good first quarter results for fiscal 2023. For starters, total revenue increased 16.9% year-over-year from $17,728 million in the same quarter last year to $20,729 million this quarter. And while noninterest income declined 13.1% YoY from $8,507 million in Q1/22 to $7,393 million in Q1/23, net interest income increased from $9,221 million in Q1/22 to $13,336 million in Q1/23 – resulting in 44.6% year-over-year growth.

Additionally, Wells Fargo reported a provision for credit losses of $1,207 million which is a lot higher than the “negative” provision for credit losses of $787 million in Q1/22. But due to lower expenses, Wells Fargo managed to increase diluted earnings per share from $0.91 in Q1/22 to $1.23 in Q1/23 – resulting in 35.2% YoY bottom line growth.

Wells Fargo Q1/23 Presentation

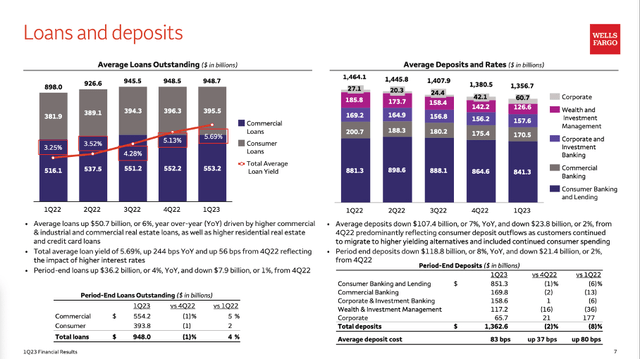

Similar to some other banks, Wells Fargo also had to report declining average deposits once again. In case of Wells Fargo, we see a constant decline over the last few quarters and average deposits declined from $1,381 billion in Q4/22 to $1,357 billion in Q1/23 (in Q1/22, average deposits were $1,464 billion).

Wells Fargo Q1/23 Presentation

And while average loans stayed the same quarter-over-quarter ($948.7 billion in Q1/23 compared to $948.5 billion in Q4/22), the number increased from $898.0 billion in Q1/22.

Financial Stability

When talking about banks and analyzing a bank, one of the most important aspects is the credit quality and financial stability. While this is always the case – it especially became obvious in March 2023 when the first banks started to fail again.

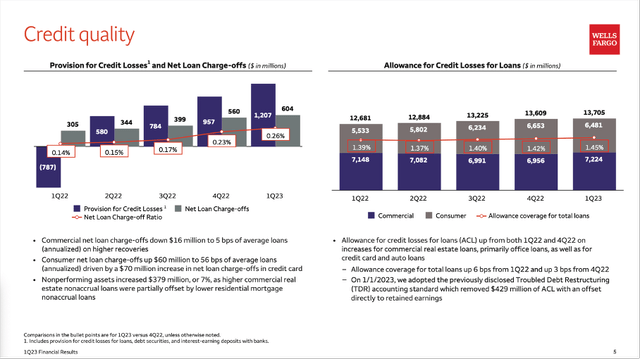

I already mentioned above that provision for credit losses increased compared to one year earlier and when looking at the chart below we also see the number constantly increasing over the last few quarters. And while building reserves is good news, it is also showing that banks – or in the case: Wells Fargo – are expecting rougher times ahead. Allowance for credit losses for loans also increased constantly over the last few quarters to $13,705 million in Q1/23. Scharf commented on the increased allowance for credit losses during the last earnings call:

We increased our allowance for credit losses for the fourth consecutive quarter. Our economic expectations used to support the allowance have not changed meaningfully, but we do continue to look at specific asset classes, such as commercial real estate to appropriately assess the adequacy of the allowance.

Wells Fargo: Credit Quality

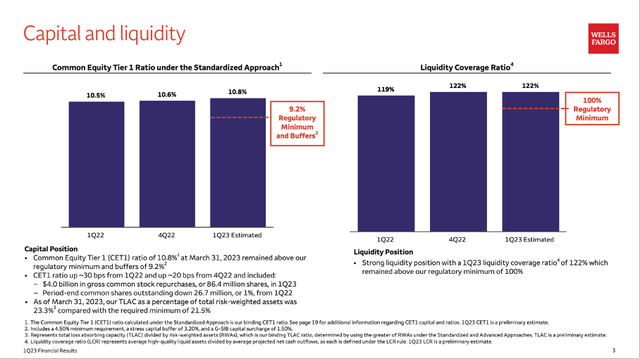

When talking about financial stability, one widely watched metric is the CET 1 ratio. In Q1/23, Wells Fargo reported a CET 1 of 10.8%, which is higher than in Q4/22 (10.6%) and Q1/22 (10.5%) and above the required regulatory minimum and buffers of 9.2%.

Wells Fargo Q1/23 Presentation

Additionally, we can look at the loan-to-deposit ratio for Wells Fargo, which was 0.70 in Q1/23 and usually a ratio below 0.8 is seen as acceptable. Wells Fargo could also report a loan-to-asset ratio of 0.51 and with ratios below 0.6 being acceptable we should also not be worried. Of course, other banks – for example most Canadian banks – can report better ratios, but by looking at these numbers Wells Fargo seems to be fine.

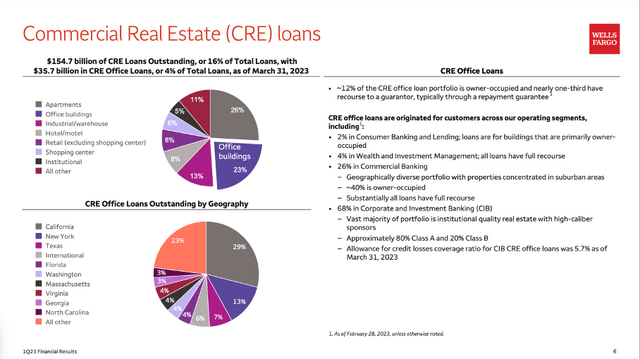

During the last earnings call, management focused particularly on the commercial real estate loans – and especially on office buildings – as management is seeing weakness here. Wells Fargo had $154.7 billion of commercial real estate loans outstanding at the end of the first quarter. Of the total loans outstanding office loans represented about 4%. Mike Santomassimo commented during the earnings call:

The office market continues to show signs of weakness due to lower demand, higher financing costs and challenging capital market conditions. While we haven’t seen this translate to meaningful loss content yet, we expect to see more stress over time.

And while the largest concentration of Wells Fargo’s office portfolio is in New York and California, management pointed out that “the vast majority of this portfolio is institutional quality real estate with high-caliber sponsors”.

Wells Fargo Q1/23 Presentation

Aside from office loans, management is also focusing on credit cards (which usually have the highest default ratio) and auto loans. Not only has the size of Wells Fargo’s auto portfolio been declining for four consecutive quarters, the origination volume declined 32% from a year ago (due to credit tightening and continued price competition). As a result, auto revenue declined 12% year-over-year to $392 million in Q1/23.

And not only auto loans are getting more problematic – consumer loans (including credits cards) are also getting worse. Wells Fargo is pointing out, that most consumers remain resilient, but for some consumer financial health is constantly weakening over the last year. Additionally, nonperforming assets also increased 7% compared to the fourth quarter (especially driven by commercial real estate).

Overall, this is not alarming so far. Of course, numbers could be better, and we are seeing warning signs. However, to get alarmed just by looking at these numbers would probably be an overreaction.

Problem: Banking System

Despite some warning signs, the financial stability of Wells Fargo does not seem to be an issue at this point. However, one problem remains – a problem I have already described in several articles in the last few months: the banking system is extremely complex, dense, and interconnected and ripple effects can occur quickly. And at least for me, it is almost impossible to see the connections between the different banks. In my article “Banking Crisis: The next domino is falling” I wrote:

While it seems obvious that several banks in a country may fail at the same time because they all bought similar assets that turned out to be worth much less than previously estimated, the spreading of a banking failure through the banking system is not so obvious at first. When a non-financial company fails this will have some consequences for suppliers as well as customers and supply chains will be disrupted a little it. But it will not cause the same ripple effect as a collapsing bank. First, the erosion of trust which is replaced by panic will spread quickly throughout the banking world. When one (or several) bank(s) start failing you will start to ask questions if your own bank is safe and might act by pulling funds. Second, as banks are lending each other money and buy assets issued by other banks countless links between banks exist and therefore problems will spread quickly through the banking system.

And a second problem is the extremely important role trust plays in the banking system. Due to several scandals in the last few years, Wells Fargo is probably not the most trusted bank (although these are two different categories of trust – one is about fraud, the other is about security and if your money is safe). But trust can erode quickly. In my article I wrote:

It is especially problematic as the situation can change within a few days: Panic can spread quickly throughout a country (or all over the world) and savers that trusted their bank last week will suddenly panic and try to withdraw funds. And therefore, it is not enough to just look at the balance sheet as many banks can be brought to their knees by a bank run and by people losing trust. A few institutions collapsing and several major headlines and reports on national television could be enough to create a panic.

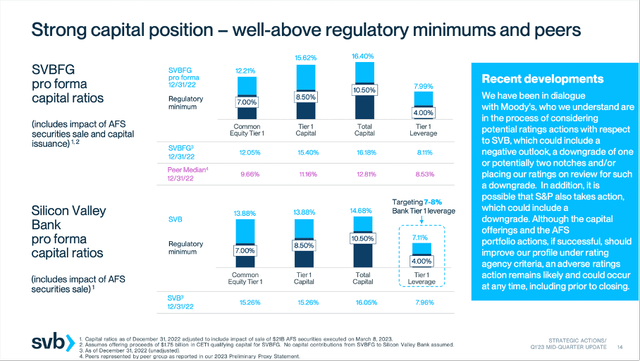

The problem is that these problems are often not visible on the surface, and it takes a lot of knowledge to identify problems before they become obvious (and it is too late). For example, a few days before Silicon Valley Bank collapsed, it reported quarterly results (including a high CET 1 ratio).

Silicon Valley Bank Q1/23 Presentation

Declining Expenses And Asset Cap

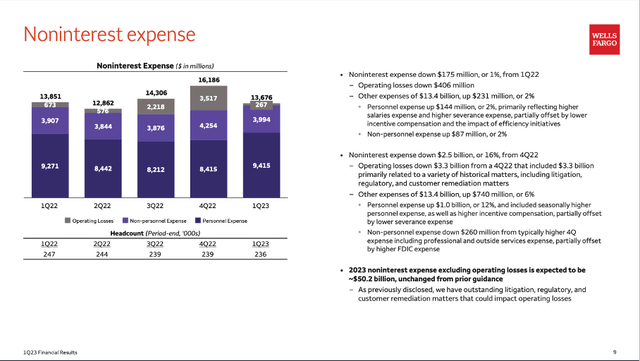

Right now, financial stability is certainly one of the most important aspects for every bank – however, efficiency and performance metrics are also important. One of the goals for Wells Fargo was to lower expenses, becoming more efficient and therefore increasing the bottom line. A way to reduce expenses is by lowering the company’s headcount – compared to one year earlier, the company reduced its headcount from 246.6K at the end of March 2022 to 235.6K at the end of March 2023. And Wells Fargo will continue to reduce the complexity and the size of the servicing book.

Wells Fargo Q1/23 Presentation

As a result, noninterest expenses continued to decline. Especially when comparing the noninterest expenses in Q1/23 to the previous quarter Q4/22, the decline is impressive but when comparing noninterest expenses to the same quarter last year, we still see a decline but a more moderate decline. Noninterest expenses declined from $13,851 million in Q1/22 to $13,676 million in Q1/23 – a decline of 1.3%. And in Q4/22, noninterest expenses were rather high due to $3.5 billion in operating losses.

We should not forget that Wells Fargo is still operating under the imposed asset cap at the size of $1.93 trillion. For more than 5 years, Wells Fargo has not been allowed to increase its total assets and it seems like the asset cap might stay till 2024. But we can assume that Wells Fargo will be more profitable once the asset cap is lifted.

Share Buybacks

In the first quarter of fiscal 2023, Wells Fargo also started share buybacks again and spent $4.0 billion on share buybacks and repurchased 86.4 million shares.

And as long as management is seeing its own stock as undervalued, using cash for share buybacks is certainly a good idea. Management also argued that due to the solid CET 1 ratio, it can spend money on share buybacks again without risking troubles. One the one hand, we can see this as a sign of strength and management being confident in its own business and the financial stability. On the other hand, we can ask the question if share buybacks are a good idea right now or if Wells Fargo should not rather focus on preserving capital considering the rough times that might be ahead.

Usually, we can interpret share buybacks as signs of confidence in the business. And although I don’t want to compare Wells Fargo to Lehman Brothers, it is worth noting that Lehman raised the dividend in 2007 as well as 2008 and bought back shares in an aggressive way till the company went bankrupt (of course, share buybacks were not the reason for bankruptcy). Therefore, buybacks alone are not proof for the business being in good shape. Sometimes, management is just stubborn or makes big strategic mistakes.

Intrinsic Value Calculation

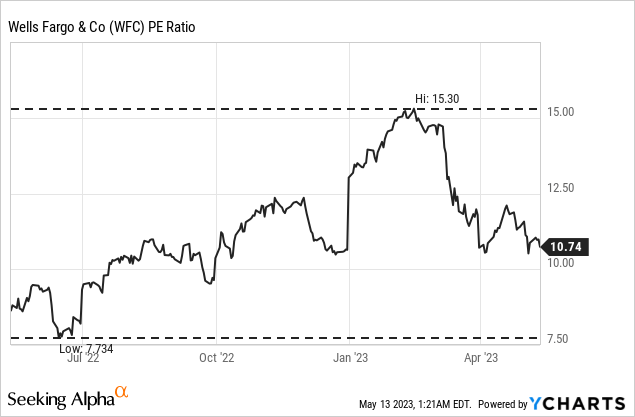

Like most other major banks (and especially many regional banks) Wells Fargo is trading for a very low valuation multiple. Earnings are (still) good, but the stock prices are depressed and as a result, Wells Fargo is trading for only about 10.5 times earnings. A few months ago, the P/E ratio was still 15.3 and the ten-year average P/E ratio is 17.64. And when using expected earnings for 2023, Wells Fargo is trading for only about 8 times forward earnings.

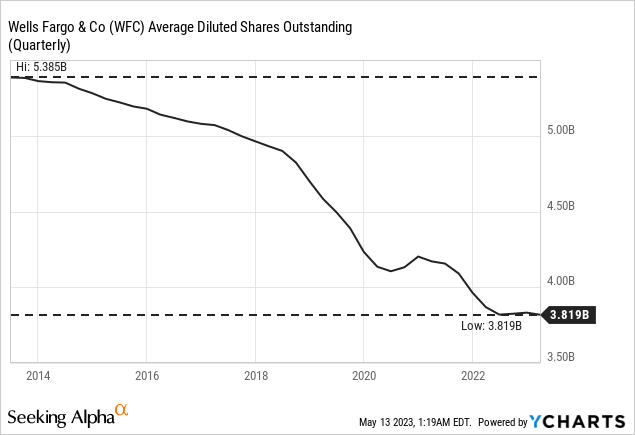

Aside from looking at valuation multiples, we can also use a discount cash flow calculation to determine an intrinsic value. Let’s be cautious and use the trailing twelve months net income of $14,385 million as basis (as well as 3,818 million outstanding shares and a 10% discount rate). Even when assuming that Wells Fargo will not be able to grow again and only able to generate a similar net income as in the last twelve months, the stock is actually fairly valued at this point (we get an intrinsic value of $37.68).

And when being a little more optimistic and assume Wells Fargo can return to previous levels ($23 billion in net income was the highest amount the company generated in the last few years), the intrinsic value would be $60.24 – once again assuming the company is not able to grow again.

Of course, Wells Fargo is not the only bank that is undervalued when calculating with such assumptions – most banks are deeply undervalued when taking the current net income and just assume 0% growth. That is just underlining how cheap banks are – but an undervalued stock is not helpful if we are facing the risk of a collapsing bank. And from a valuation standpoint, most major banks in the United States and Canada can be bought right now – and most will be a good investment (aside from those banks collapsing and getting suddenly into serious troubles). And it is hard to know which banks this will be – that is the main problem right now and the reason I don’t want to invest in banks.

Conclusion

Up until now, it is mostly regional banks that are affected and collapsing. Nevertheless, I would still be very cautious, and I don’t want to invest in any bank at this point. Of course, there is always the risk of missing a good investment opportunity as several banks are really cheap right now. But the risk of further banks collapsing is rather high at this point – and it is extremely difficult to foresee which bank might be the next in line.

And while not every bank is facing the risk of failure and bankruptcy, steeply declining earnings are a real risk. So far, first quarter results were quite good for most banks, but with earnings declining in the coming quarters, the risk of further declining stock prices is also high.

")

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/xlmedia/X67Z7GJHNNBGDAEUDWTNYQMC4E.jpg "Man United Premier League 2022/23 season review")